Rent vs Buy a Home in 2026: The Hidden Wealth Gap Most People Overlook

Rent or Buy? The Real Tradeoff Most People Don’t Talk About

Should you rent or buy a home in today’s market? Discover the long-term financial impact, wealth-building benefits of homeownership, and what renting really costs over time.

You’ve probably found yourself wondering lately: Is buying a home even worth it right now? You’re not alone. With rising home prices and fluctuating mortgage rates, this question has become more common than ever.

At first glance, renting can seem like the simpler, more manageable choice. In some situations, it may even feel like the only realistic option. And honestly, if that’s where you are, that’s completely valid.

But when comparing renting and buying, there’s one critical angle that often gets overlooked.

What does each choice mean for your future?

What Renting Really Gets You (And What It Doesn’t)

Depending on your lifestyle and financial situation, renting definitely has its perks:

Lower upfront costs compared to buying

Minimal maintenance responsibilities

Flexibility to relocate more easily

These advantages make renting appealing—especially for those who prioritize mobility or are still building financial stability.

However, there’s a growing concern among renters. A survey by Bank of America found that 70% of aspiring homeowners worry about the long-term impact of renting.

And that concern comes down to one key issue: lack of ownership and wealth building.

As Yahoo Finance explains:

“Paying rent doesn't build equity. You get a place to live, but no ownership stake, no price appreciation, and no asset to leverage for future borrowing or investment.”

In simple terms, rent payments provide a roof over your head—but they don’t contribute to your financial growth.

So while renting may offer convenience today, that convenience comes with a long-term tradeoff.

How Homeownership Builds Wealth Over Time

On the other side of the equation is homeownership—one of the most reliable ways to build wealth over time.

Why? It all comes down to equity.

Equity is the difference between your home’s market value and what you still owe on your mortgage. Every payment you make increases your ownership stake. And as property values rise, your equity can grow even faster.

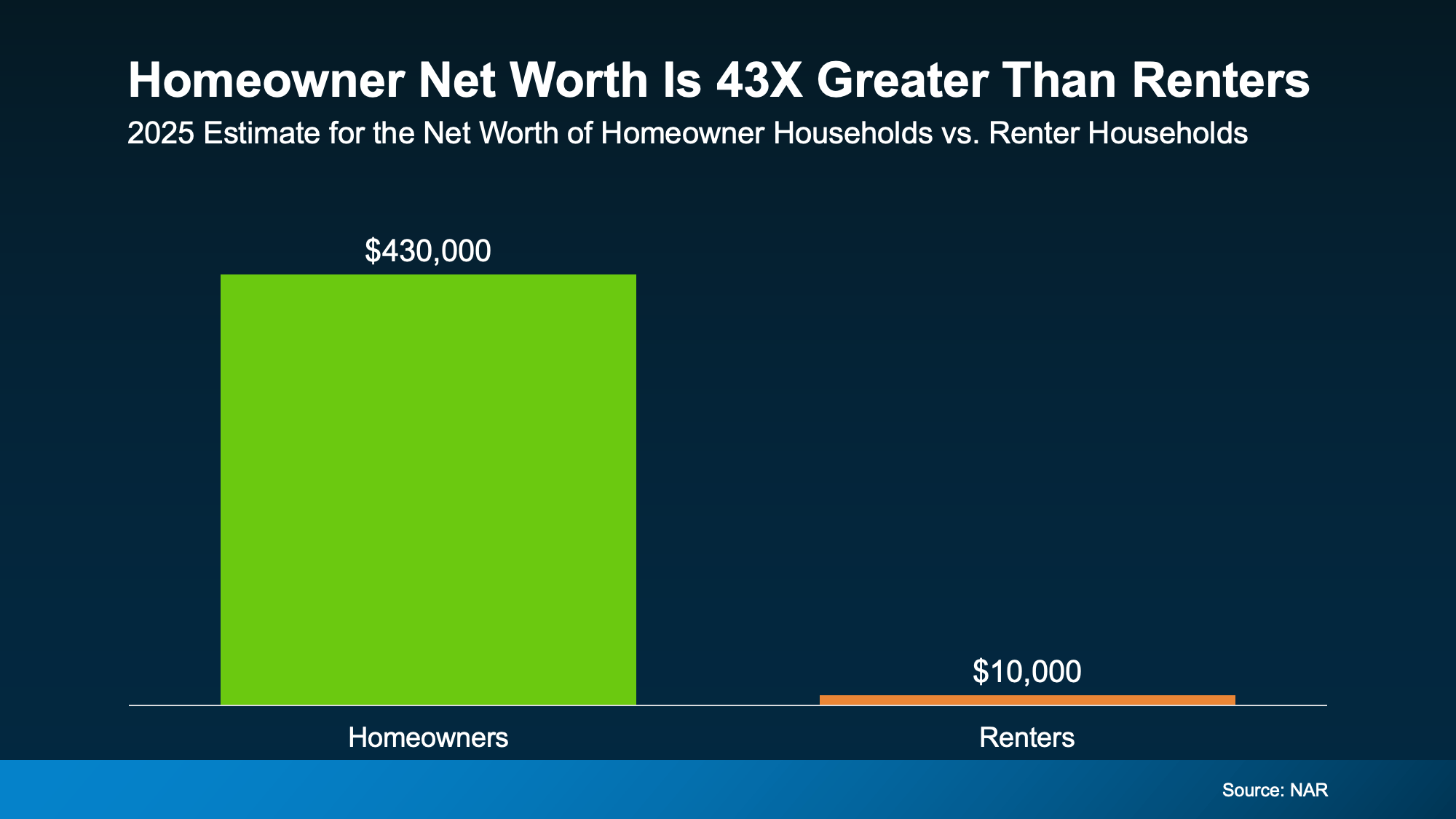

According to the National Association of Realtors (NAR), the average homeowner’s net worth is 43 times greater than that of a renter.

Here’s how it breaks down:

Homeowners: $430,000 average net worth

Renters: $10,000 average net worth

That’s not a small gap—it’s a massive financial divide.

And it’s not because homeowners necessarily earn more or make better day-to-day decisions. The difference lies in the long-term impact of owning an appreciating asset.

Think of it this way:

Owning a home is like having a savings account you live in.

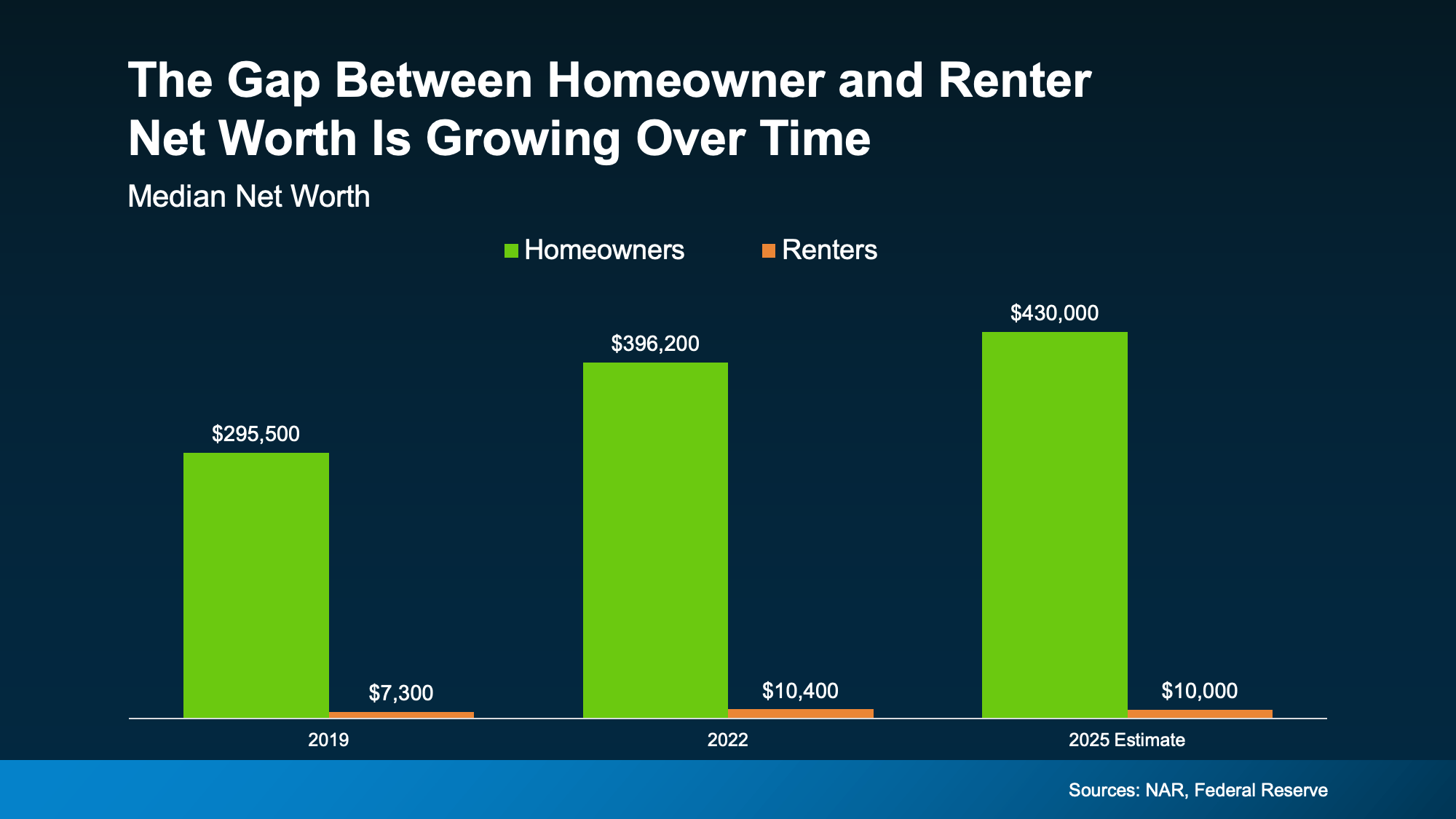

The Wealth Gap Between Renters and Owners Is Growing

What’s even more striking is that the gap between renters and homeowners isn’t shrinking—it’s expanding.

Over the years, data consistently shows that homeowners continue to build wealth while renters remain financially stagnant in comparison.

Even in 2025, when housing prices began to stabilize, homeowners still experienced growth in their net worth. This trend highlights an important reality:

Real estate remains a long-term wealth-building tool—even during market shifts.

Here’s the underlying truth many people overlook:

When you rent, you’re contributing to your landlord’s wealth.

When you own, your payments build your own financial future.

So the real question becomes:

Whose equity do you want to build—yours or someone else’s?

So, Should You Buy a Home Right Now?

The honest answer? It depends.

While the long-term advantages of buying a home are clear, that doesn’t automatically mean now is the right time for everyone.

Here are a few factors to consider:

Are your finances stable?

Do you have savings for upfront costs?

Are you ready for the responsibilities of homeownership?

Do you plan to stay in one place for several years?

If the answer to most of these is yes, buying may be closer than you think.

If not, that’s okay too. Renting can serve as a stepping stone while you prepare.

What matters most is having a plan.

A conversation with a local real estate expert can help you:

Understand your budget

Explore financing options

Set a realistic timeline

Identify what steps you need to take next

Clarity removes uncertainty—and helps you move forward with confidence.

The Bigger Picture: Short-Term Ease vs Long-Term Gain

At its core, the rent vs buy decision comes down to short-term flexibility versus long-term wealth building.

Renting offers:

Convenience

Lower commitment

Short-term affordability

Buying offers:

Equity growth

Long-term financial stability

Ownership and control

Neither choice is inherently wrong—but they lead to very different financial outcomes over time.

Bottom Line

Renting might feel more manageable right now—and for many people, it’s the right choice in the moment.

But over time, it can come at a cost: missed opportunities to build wealth and financial security.

If your goal is to move beyond renting and start investing in your future, the first step is simple:

Start the conversation.

Explore your options.

Create a plan.

Because the sooner you understand your path, the sooner you can decide when buying makes sense—not just wonder if it ever will.