Thinking About an Adjustable-Rate Mortgage? Here’s What You Need To Know

Adjustable-Rate Mortgage (ARM) Guide 2026: Pros, Cons, and Smart Homebuyer Strategies

Learn everything about adjustable-rate mortgages (ARMs) in 2026. Discover how they work, their pros and cons, and whether an ARM is the right choice for your homebuying strategy.

If you’ve been looking for a home lately, you’ve probably felt how tough affordability still is. Rising home prices, elevated interest rates, and tighter lending conditions have made it more challenging for many buyers to enter the market. And that's exactly why more buyers are opting for adjustable-rate mortgages, or ARMs.

In today’s dynamic housing market, flexibility is becoming just as important as stability. Buyers are exploring creative financing options, and ARMs are stepping back into the spotlight as a viable solution.

Here's what you need to understand about how they work, and whether they make sense for you.

What Is an Adjustable-Rate Mortgage?

Since a lot of people aren’t familiar with this type of loan, let’s start with a definition. This is how Business Insider explains the main difference between a fixed-rate mortgage and an adjustable-rate mortgage:

“With a fixed-rate mortgage, your interest rate remains the same for the entire time you have the loan. This keeps your monthly payment the same for years . . . adjustable-rate mortgages work differently. You’ll start off with the same rate for a few years, but after that, your rate can change periodically. This means that if average rates have gone up, your mortgage payment will increase. If they’ve gone down, your payment will decrease.”

Basically, one doesn’t change much over the life of your loan.

And one could change... either by a little, or a lot.

Of course, things like taxes or homeowner’s insurance can still have an impact on a fixed-rate loan, but the baseline of your mortgage payment is fairly steady. But the big difference is that with an ARM, your monthly payment could change over time.

How ARMs Typically Work

Most adjustable-rate mortgages follow a structure like 5/1, 7/1, or 10/1 ARMs. This means:

The first number = fixed-rate period (e.g., 5 years)

The second number = how often the rate adjusts after that (e.g., every year)

For example, a 5/1 ARM has a fixed interest rate for five years, then adjusts annually.

This structure makes ARMs appealing for buyers who don’t plan to stay in their home long-term.

Why Adjustable-Rate Mortgages Are Getting More Attention

So, why do some buyers choose this option? It's simple. It’s because of the upfront savings. Business Insider explains it like this:

“Because ARM rates are typically lower than fixed mortgage rates, they can help buyers find affordability when rates are high. With a lower ARM rate, you can get a smaller monthly payment or afford more house than you could with a fixed-rate loan.”

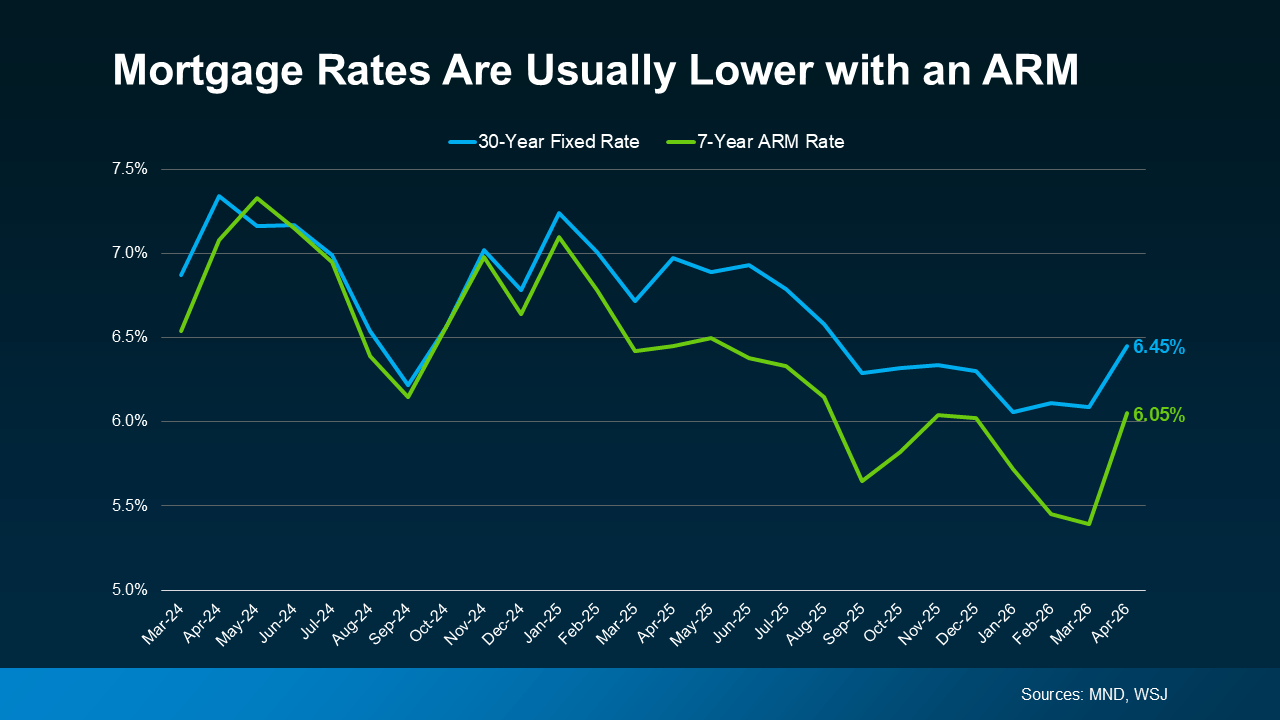

And right now, according to Mortgage News Daily and the Wall Street Journal, the upfront rate on an ARM is lower than a 30-year fixed mortgage.

If you’re wondering how that shakes out in real dollars and cents, here’s what Redfin says. According to their research, the typical buyer could save about $150 per month by taking out an ARM instead of a 30-year fixed mortgage.

For some people, that’s enough to make a difference.

Real-World Impact of Lower Rates

Let’s break that down:

A lower monthly payment can improve cash flow

Buyers may qualify for higher-priced homes

Savings can be redirected to investments or renovations

In high-cost housing markets, even small monthly savings can significantly impact long-term financial planning.

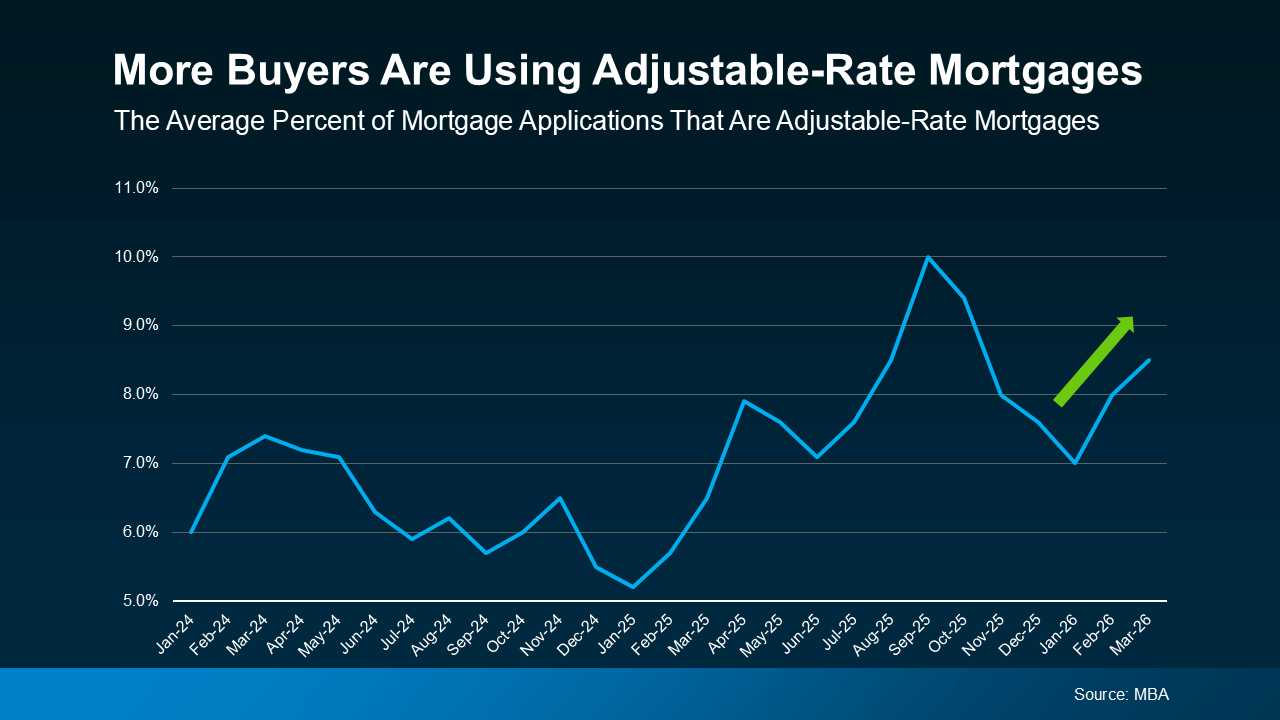

More Buyers Are Choosing Adjustable-Rate Mortgages Today

A growing number of buyers are willing to trade the uncertainty later for a lower payment now. Data from the Mortgage Bankers Association (MBA) shows the share of buyers choosing ARMs has increased, especially over the last few years.

This doesn’t mean ARMs are becoming the go-to option for everyone. It only means some buyers are opting for this type of mortgage, so they can still buy today.

And if you remember the housing crash, seeing ARMs gain popularity again may raise concerns. But rest easy. Today’s ARMs aren’t the same.

Back then, some buyers were given loans they couldn’t afford once rates adjusted.

Today, lending standards are stricter, and lenders evaluate whether borrowers could still handle the payment if rates rise. So, the return of ARMs doesn’t signal another widespread crash. It just reflects how some buyers are adapting to today’s affordability challenges.

Key Improvements in Modern ARMs

Stricter borrower qualification requirements

Caps on how much interest rates can increase

Better transparency in loan terms

More regulated lending practices

These safeguards help reduce the risks that were common in the past.

The Trade-Off – What You Need To Consider

If you’re considering an adjustable-rate mortgage yourself, just remember it really all depends on your situation and your risk tolerance.

An ARM may make sense if you plan to move before your rate would adjust or if you expect you’ll make a higher income in the future. But there are trade-offs you need to think through.

For example, once the fixed period ends, your rate can adjust, and your payment could increase, potentially by a meaningful amount depending on where rates are at that time.

And keep in mind, there’s also no guarantee mortgage rates will come down in the future, which means refinancing later isn’t always an option. That’s why it’s important to think through your plan, understand your long-term earning potential, and work closely with a trusted lender before you choose an ARM.

Pros and Cons of ARMs

✅ Pros:

Lower initial interest rates

Reduced monthly payments early on

Greater buying power

Ideal for short-term homeowners

⚠️ Cons:

Unpredictable future payments

Potential for higher long-term costs

Market-dependent rate adjustments

Refinancing is not guaranteed

Who Should Consider an ARM?

An adjustable-rate mortgage may be a smart choice if you fall into one of these categories:

Short-term homeowners: Planning to move within 5–10 years

Career growth expected: Anticipating higher income soon

Investors: Looking to maximize short-term cash flow

Rate watchers: Expecting interest rates to drop in the future

However, if you prefer stability and predictability, a fixed-rate mortgage might still be the better option.

Expert Tips Before Choosing an ARM

Before committing to an adjustable-rate mortgage, consider these practical tips:

Understand rate caps: Know how much your rate can increase

Review adjustment intervals: Annual vs. semi-annual changes

Stress-test your budget: Can you afford higher payments?

Have an exit strategy: Plan to sell or refinance if needed

Consult professionals: Speak with a lender or financial advisor

Taking these steps can help you avoid surprises and make a more confident decision.

Bottom Line

ARMs are getting more attention again because they can make buying a home more affordable in the short term. But they’re not right for everyone.

The key is understanding how they work, what the risks are, and whether they fit your plan. And that’s why you need to talk to a trusted lender and financial advisor before you make any decisions.

Final Thoughts

In a market where affordability remains a challenge, adjustable-rate mortgages offer a flexible alternative for certain buyers. But like any financial decision, they come with trade-offs.

The smartest move isn’t choosing what’s popular—it’s choosing what aligns with your financial goals, timeline, and comfort with risk.

If you approach ARMs with a clear strategy and the right guidance, they can be a powerful tool in your homeownership journey.