Do You Need 20% Down to Buy a Home in Central Florida? What First-Time Buyers Should Know in 2026

The Truth About Down Payments: Why Many Central Florida Buyers Can Purchase Sooner Than They Think

Think you need 20% down to buy a home in Central Florida? Learn the truth about down payment options, local buyer programs, FHA, VA, USDA loans, and how first-time buyers can purchase sooner in Orlando, Tampa, Lakeland, and beyond.

Many future homeowners across Central Florida delay buying because they believe they need a 20% down payment before they can purchase a home.

That idea has been repeated for years—but for many buyers, it simply isn’t true.

If you're renting in places like Orlando, Lakeland, Winter Haven, Tampa, Kissimmee, or Ocala and waiting to save 20%, you may be postponing homeownership longer than necessary.

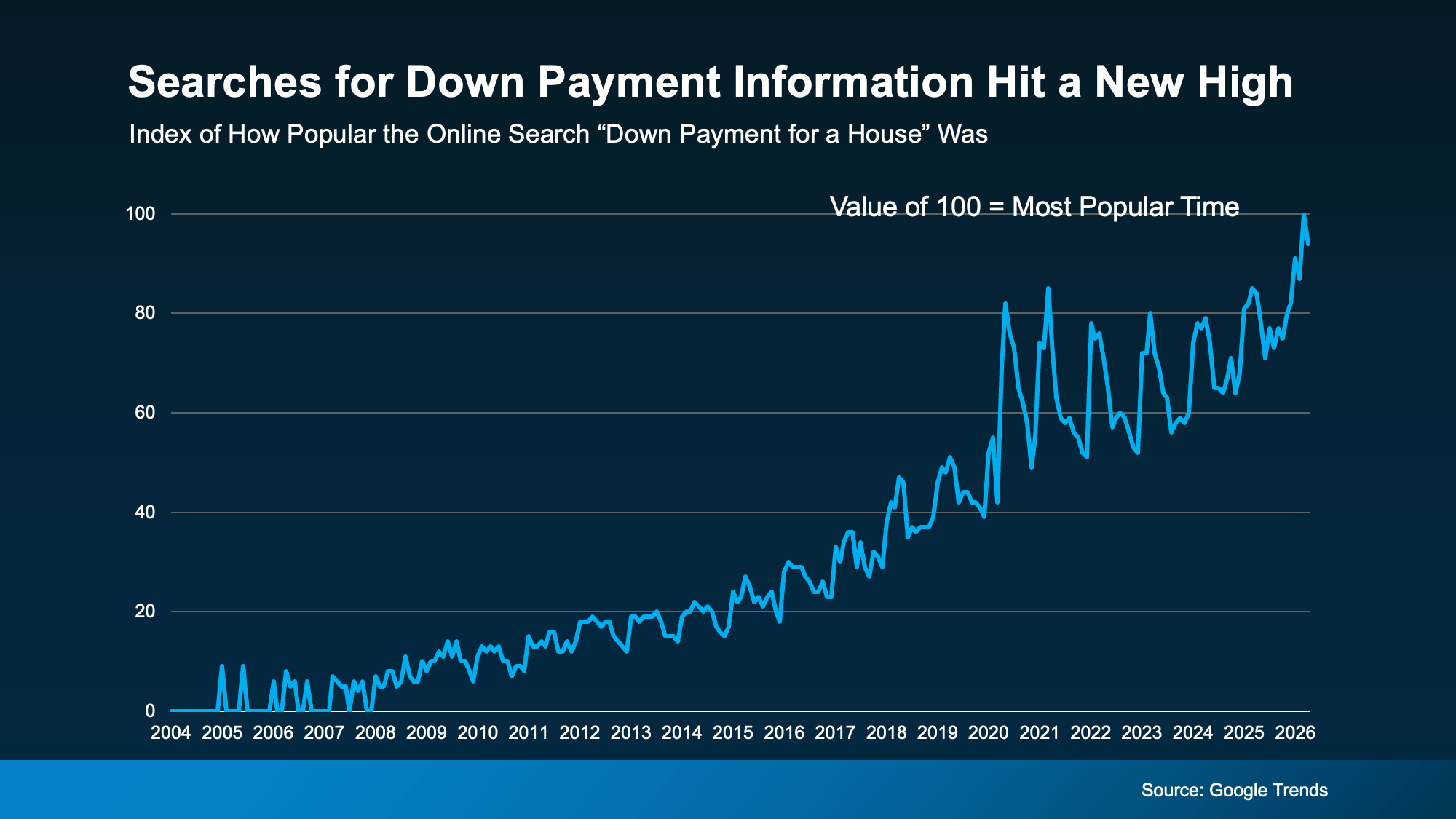

According to Google Trends, online searches for down payment information recently hit an all-time high. And that’s a clear sign more buyers are trying to figure out what they really need to save before making a move (see graph below):

The truth is this: many first-time homebuyers purchase with much less down depending on their loan type, credit profile, income, and eligibility. National housing data shows first-time buyers often put down single-digit percentages rather than 20%.

Let’s break down what Central Florida buyers need to know right now.

Where Did the 20% Down Payment Myth Come From?

The 20% number became popular because it can help buyers:

Avoid private mortgage insurance (PMI) on many conventional loans

Lower monthly mortgage payments

Reduce total loan amount

Improve financing flexibility

Those are real advantages—but they are benefits, not requirements.

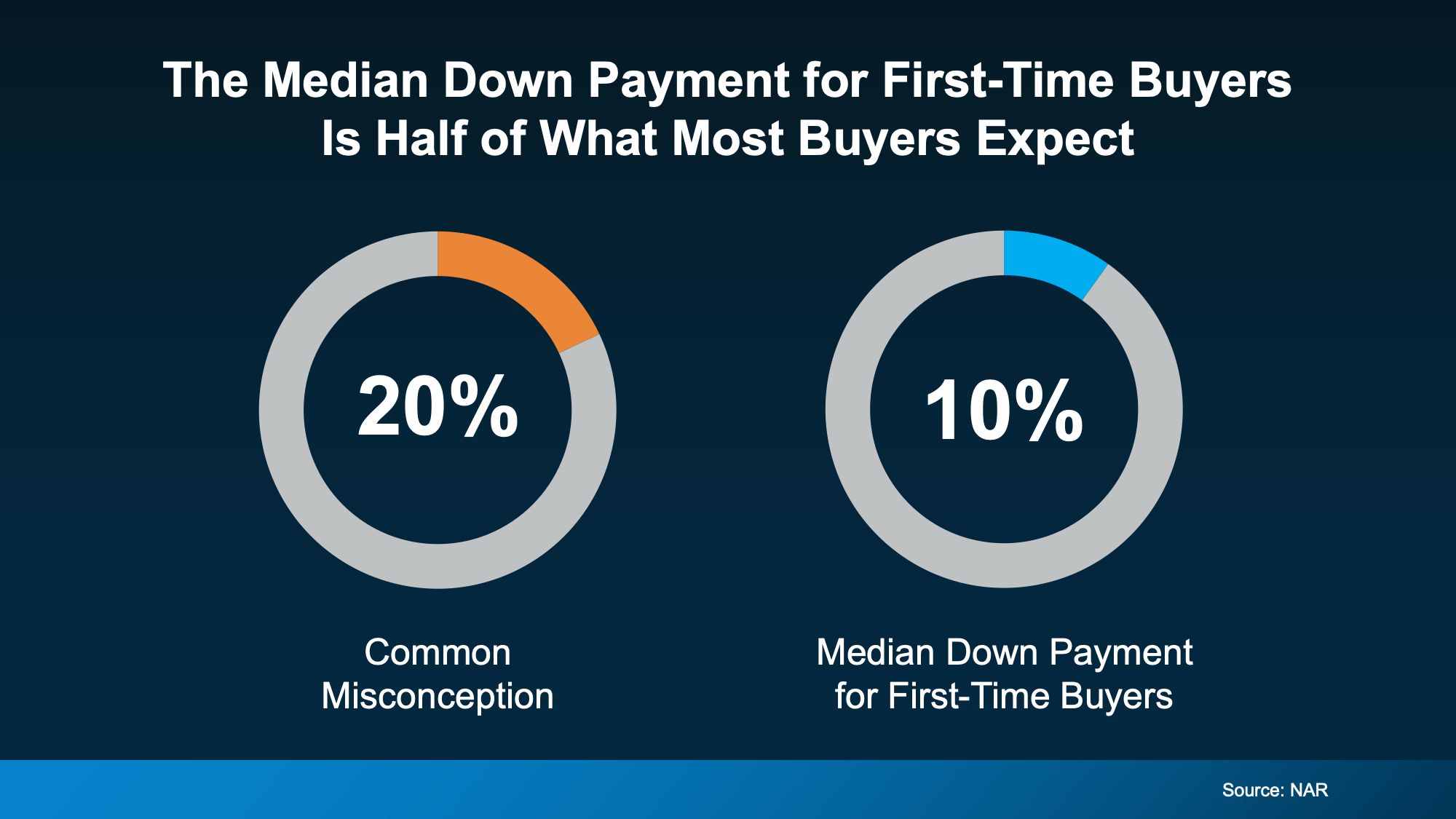

According to the National Association of Realtors (NAR), the median down payment for first-time homebuyers is only 10%. That’s half of what you probably expected.

Today’s lending market offers multiple paths to homeownership with lower upfront cash needs.

For many Central Florida buyers, especially first-time purchasers, waiting until they save 20% could mean:

Paying rent for several more years

Missing equity growth opportunities

Facing higher home prices later

Competing in a different rate environment

How Much Down Payment Do Buyers Really Need?

Depending on the loan program, buyers may qualify with significantly less than 20%.

Conventional Loans

Some conventional loan programs allow qualified buyers to purchase with as little as 3% down.

Best for buyers with:

Stronger credit

Stable income

Lower debt-to-income ratios

FHA Loans

FHA loans commonly allow 3.5% down for qualified buyers.

Popular among:

First-time buyers

Buyers rebuilding credit

Buyers needing more flexible approval guidelines

VA Loans

Eligible veterans, active-duty service members, and some surviving spouses may qualify for 0% down VA financing.

USDA Loans

Certain rural and suburban areas surrounding Central Florida may qualify for 0% down USDA loans, depending on location and income eligibility.

Why This Matters in Central Florida

Central Florida continues to attract residents because of:

Job growth

Tourism-related employment

Healthcare expansion

Logistics and distribution hubs

Warm climate lifestyle

No state income tax in Florida

That demand can keep pressure on housing prices in desirable communities.

If you wait several years trying to save a full 20%, you could face:

Higher purchase prices

Increased insurance costs

More expensive rents

Reduced affordability overall

Sometimes buying with a smaller down payment sooner can outperform waiting for a larger down payment later.

Example: Waiting Could Cost More Than PMI

Many buyers avoid lower down payment options because of mortgage insurance.

But here’s the bigger picture:

If rent is $2,000 per month and you wait two more years to save 20%, that’s roughly $48,000 in rent payments—money that does not build ownership equity.

Meanwhile, if home values rise during that time, your target down payment may rise too.

In many cases, a modest PMI payment may be less costly than delaying ownership for years.

Every buyer’s math is different, but this is why strategy matters more than myths.

Central Florida Areas Where First-Time Buyers Still Find Opportunity

While some neighborhoods are premium-priced, many buyers still find value in surrounding areas.

Greater Orlando Area

Clermont, Apopka, Sanford, and Kissimmee often attract buyers seeking more affordability than core Orlando neighborhoods.

Polk County Growth Corridor

Lakeland, Winter Haven, and nearby communities remain popular for commuters between Orlando and Tampa.

Tampa Commuter Markets

Areas east of Tampa may offer opportunities for buyers who want more space.

North Central Florida Options

Ocala continues to draw buyers seeking affordability and land.

Don’t Forget Down Payment Assistance

Many buyers assume their only option is saving everything themselves.

That’s not always true.

Some buyers may qualify for:

State housing assistance programs

County or city grants

Forgivable second mortgages

Closing cost assistance

First-time buyer education incentives

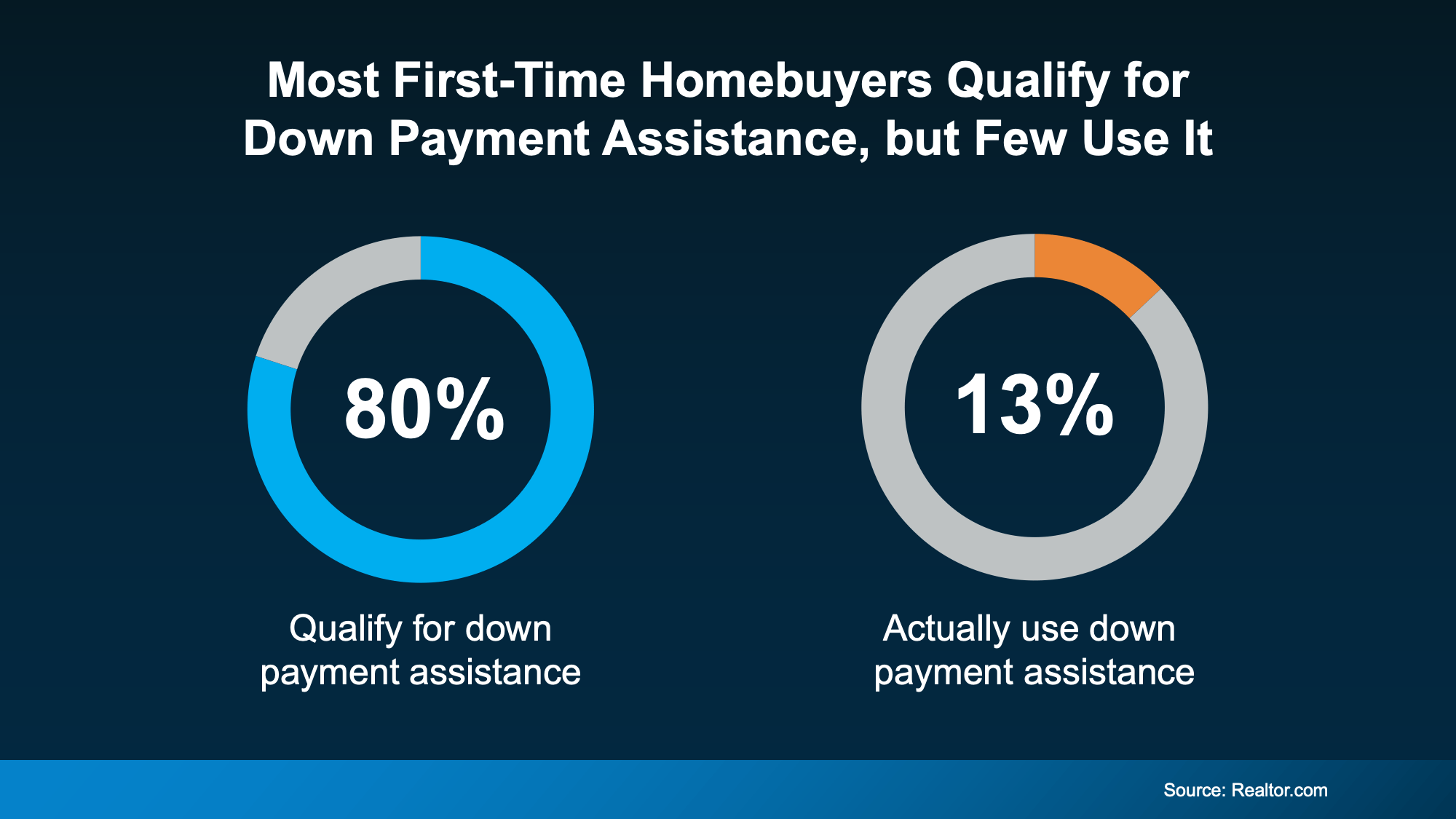

Research from Realtor.com shows almost 80% of first-time homebuyers qualify for down payment assistance (DPA), but only 13% actually use it (see chart below):

A local lender can help identify options specific to Central Florida counties.

What You Should Do Before You Start House Hunting

1. Talk to a Local Lender First

Get pre-approved before browsing homes seriously. This gives you:

Realistic monthly payment targets

Estimated cash-to-close numbers

Loan program options

Confidence when making offers

2. Focus on Monthly Payment, Not Just Down Payment

Sometimes buyers obsess over down payment size while ignoring:

Taxes

Insurance

HOA dues

Utilities

Maintenance reserves

Affordable ownership is about the full picture.

3. Work With a Local Real Estate Expert

A Central Florida agent can guide you on:

Neighborhood value trends

Insurance-sensitive areas

Commute patterns

New construction opportunities

Negotiation strategy

The Bottom Line

You do not automatically need 20% down to buy a home in Central Florida.

For many buyers, the right path may be:

3% down conventional financing

3.5% down FHA

0% down VA or USDA

Down payment assistance programs

If you’ve been waiting because of an outdated rule, now may be the time to explore what’s actually possible.

The smartest next step is to speak with a trusted local lender and real estate professional who understands the Central Florida market—and can show you real numbers instead of myths.